Insights

Private Debt in Small and Medium-Sized Enterprises (SMEs): Growth, Opportunity and the Role of Fair Value in Risk Management

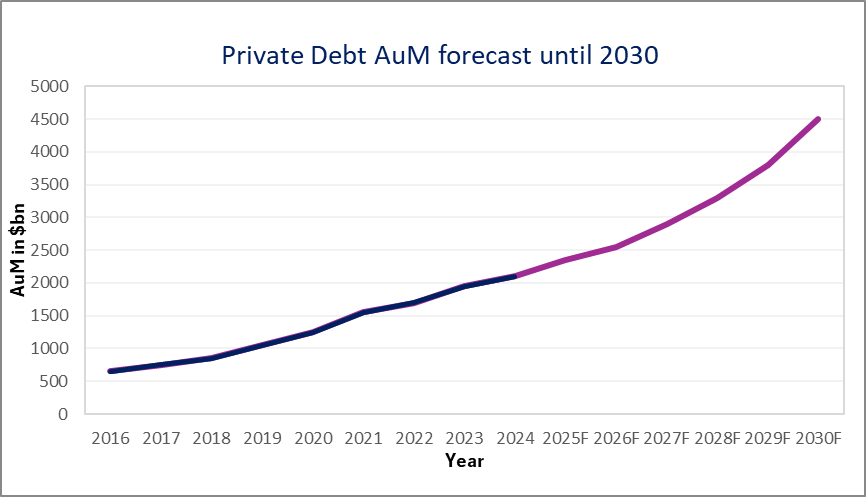

Private Debt in SMEs – Growth and Rising Requirements

Since the global financial crisis, the financing landscape for small and mid-sized enterprises (SMEs) has undergone a profound transformation. Stricter regulatory capital requirements and evolving supervisory expectations have led many banks to reassess traditional lending activities. While banks remain central to SME financing, balance-sheet constraints and a more selective risk appetite have increasingly shifted parts of corporate lending towards non-bank providers. Private debt has therefore emerged as an important and complementary source of financing for SMEs.

Over the past decade, private debt has evolved from a niche alternative into a well-established institutional asset class with steadily rising assets under management and increasingly professionalized fund structures. Investors are attracted by predictable cash flows, downside protection and diversification benefits relative to public markets. As shown by the rapid growth in private debt volumes, the market has become a key pillar of modern corporate financing.

This development represents a clear opportunity for the real economy. At the same time, the growing relevance of private debt has raised expectations regarding transparency, governance and valuation discipline. Recent coverage in leading German business media has reflected these expectations by highlighting discussions around risk assessment and valuation practices in private credit markets.¹ In this context, robust fair value frameworks are particularly important in a market characterized by limited liquidity and individually structured transactions, as they support informed decision-making and sustainable market development.

¹Handelsblatt, Antonia Mannweiler, “Kreditboom ohne Banken“, print edition dated 05.02.2026, pp.28-29.

Growth Opportunities and Structural Drivers of Private Debt

The expansion of private debt is underpinned by structural drivers that are particularly relevant for SMEs. Many operate in specialized niches, pursue long-term growth strategies and seek financing partners who understand their business models, cash-flow dynamics and strategic objectives.

Private debt lenders are well positioned to meet these needs. Financing solutions can be tailored in terms of seniority, amortization profiles, maturities and covenant structures, enabling borrowers to align debt service obligations with operational cash flows and investment cycles. This flexibility supports SMEs undergoing expansion, succession planning or strategic transformation.

From an investor perspective, private debt offers attractive risk-adjusted returns, supported by an illiquidity premium that compensates for long-term capital commitment, detailed underwriting and active monitoring. Beyond individual transactions, private debt also plays an important macroeconomic role by complementing bank lending and supporting continued investment and innovation in the SME sector.

With Growth Comes Complexity: Key Risk Dimensions in Private Debt

As private debt markets expand, transaction complexity increases. Refinancing and liquidity risks can arise when financing conditions tighten or maturities approach. In such situations, lenders may rely on refinancing by new providers, partial repayment through asset disposals or sponsor-led solutions, all of which are sensitive to prevailing market conditions. Rising refinancing risk typically translates into higher required credit spreads and directly affects discount rates in fair value assessments.

Covenant risks may build gradually but often materialize abruptly once thresholds are breached, potentially accelerating refinancing needs. Rising interest rates and shifting risk premiums can introduce valuation volatility that may not be immediately visible in book values. While amortised cost carrying values are largely based on contractual cash flows, fair value incorporates forward-looking assumptions on refinancing feasibility and risk-adjusted discounting, making it more responsive to emerging credit and market risks.

Contractual features such as ratchet clauses further increase complexity. Where margins adjust based on leverage or other performance metrics, fair value assessments must model the evolution of these drivers over the life of the instrument. Higher leverage typically implies weaker debt quality, higher margins and higher required credit spreads, all of which must be reflected consistently in valuation models.

These factors do not diminish the attractiveness of private debt, but underscore the importance of professional risk management supported by robust valuation processes.

Valuation as a Central Steering and Early-Warning Tool in Private Debt

Fair Value as Governance and Steering Tool

In private debt markets, fair value determination has become a central element of professional investment governance rather than a purely technical reporting exercise. Robust valuation frameworks are essential to ensure that portfolio values reflect economic reality in an asset class characterized by limited liquidity and infrequent observable market prices.

Supervisory authorities have increasingly emphasized the need for sound valuation and risk management frameworks in alternative investment segments. BaFin has highlighted that the growing relevance of private debt requires enhanced transparency and sound governance, particularly in less liquid and complex environments.²

Regular and well-founded valuations provide critical transparency across the investment lifecycle. They enable investors and fund managers to consistently assess debt quality, downside exposure and changing market conditions at an early stage. In an environment of rising interest rates, shifting risk premiums and increasing refinancing pressure, timely valuation insights are indispensable for informed portfolio steering and capital allocation decisions.

From a valuation perspective, several key parameters are particularly sensitive and therefore require frequent recalibration. These include discount rates and credit spreads, forward-looking cash-flow assumptions and recovery expectations. Even small changes in these inputs can materially affect valuation outcomes.

For SMEs, fair value analysis can act as an early-warning mechanism by identifying refinancing risks or covenant pressure before they materialize in financial distress. For investors, this supports proactive engagement and timely intervention.

² BaFin, speech by Executive Director Julia Wiens at the Institute for Insurance Law, Düsseldorf, May 14, 2025.

Independent Valuation

For private debt funds, consistent fair value determination is also a key prerequisite for transparent communication with limited partners, auditors and supervisory bodies. Independent fair value processes enhance comparability across funds and vintages, reduce the risk of delayed value adjustments in stress phases and strengthen confidence in reported NAVs.

An independent valuer is a valuation function that is organizationally and economically separate from portfolio management and investment decisions. Independent valuers apply consistent, market-based methodologies and are not influenced by transaction execution or performance incentives. This distinguishes them from internal valuation models, which support portfolio monitoring and decision-making but are more closely aligned with investment perspectives.

Importantly, fair value should not be understood as a purely model-driven output. Based on defined assumptions the fair value provides a structured analytical reference to the economic value, which reflects the price a market participant would pay under current conditions, incorporating liquidity constraints, refinancing feasibility and prevailing market sentiment.

When applied consistently and embedded in governance frameworks, fair value becomes a shared analytical language between investors, fund managers and borrowers. It reduces information asymmetries, supports disciplined risk management and contributes to the resilience of private debt portfolios across market cycles. Rather than constraining investment activity, robust valuation practices enable private debt to realize its full potential as a stable and responsible asset class.

Implications for Investors and Market Participants

The growth of private debt brings rising expectations for governance and valuation discipline. For institutional investors, robust valuation frameworks are a core element of fiduciary oversight. For asset managers, valuation must be embedded in portfolio monitoring and investment decision-making rather than treated as a downstream reporting task.

Transparent and independently supported valuation practices enhance confidence in reported NAVs and strengthen long-term capital allocation decisions. For borrowers, valuation-based communication can improve dialogue with lenders and facilitate earlier, value-preserving solutions in periods of stress.

Independent valuers play a distinct role by providing an external reference point that complements internal valuation models. Organizational separation from portfolio management helps reinforce objectivity, particularly in volatile markets when assumptions are most sensitive. By challenging key inputs such as discount rates, refinancing scenarios and recovery expectations, independent valuation strengthens credibility and reduces the valuation lag.

Conclusion and Outlook

Private debt in SMEs represents a significant opportunity for companies, investors and the broader economy. Its growth reflects structural shifts in corporate financing and increasing demand for flexible, long-term capital solutions.

As the market matures and structures become more individualized, complexity and risk naturally increase. Professional risk management and robust fair value determination are therefore central enablers of a sustainable market development. Looking ahead, a continued focus on valuation discipline, governance and transparency will help ensure that private debt remains a resilient institutional asset class supporting long-term value creation in the real economy.

Featured Insights

PRIIPs arrival price: will non-compliance put your reputation at risk

Gil Bender, CEO at Value & Risk, examines how recent changes to PRIIPs rules will impact fund managers and ...